The atmosphere of stock trading is cyclic and seasons come and go like in our real life. But there are some differences. You know well when the winter season will come and end. Likewise, you know about every season like the summer, spring or rainy seasons. In stock trading you don’t know when the spring will come and go. But if you are a seasoned trader you must be knowing as which season traders are in nowadays. And even while you come to know about your trading season with some degree of certainty it is really impossible to predict which day will be normal and which choses to be an aberration for the declared season. And the patches of aberrations can be so long that you begin to believe that actually the season has changed wholly. The moment you take a move befitting to your assessed season indices you are forced to believe that the declared season has not passed away and is here to stay much longer to an indefinite period.

While

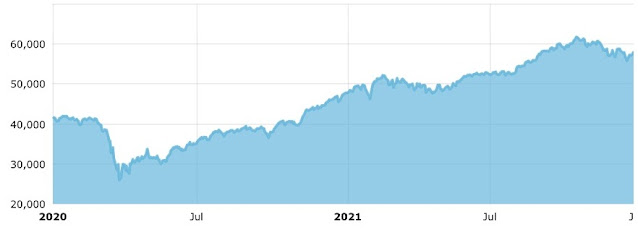

analysing the sensex graph I had concluded that pre-pandemic level i.e. March

2020 was a sane level of around 41000 which was arrived through reasonable pace

of rally. Though the pace of Sensex during 2008-2020 seemed somewhat slothful

but it could be said reasonable in view of the almost depression like situation

prevailing all around the world. And in March 2020, at the onslaught of Corona, this index took a nosedive to

28000 level which was well expected. Thenafter it was expected to rise

gradually to some notches around 40000. But what happened was mesmerising. It

went up and up and up for 20 months in a row though of course with some intermittent

and insignificant slips. The only logic behind it was the positive sentiment of

people that the world will not last in corona and quite a large number of

people will survive even after it. And when the vaccination came, the

sentiment of the people at large was as if in revelry. Many shops remained

closed, many factories stopped production during the covid menace. So the

people were left with negligible choices to spend money. More money remained

unspent and this led to rise in phenomenal liquidity. This added with the

victorious sprit over corona added to the somewhat insane upward movement of the

Sensex from 28000 level to 61923 just in 19 months.

Then I

thaught that well if it has risen to the Everest level then it must climb down

soon and fast. Though I am still confident that it will come down to a reasonable

level of around 50000 in line with the annual 10%

growth like 40000 to 44000 and then to 48400. See, I have already taken 10% CAGR in

place of the usual 6% that is taken for a developing country like India still

it is looking like a far cry. The monkey will come down but when only God knows

it better.

.......

Author - Hemant K Das

Email - hemantdas2001@gmail.com

Nice insights and target views. Congratulations 🎉

ReplyDeleteThanks a lot Vijay!

Delete